Roth Conversions Before RMDs in Retirement

If you have a large traditional IRA, your biggest tax problem in retirement may not show up until your 70s.

That is the part many retirees miss. For years, everything can look fine on paper. Your spending is covered. Social Security is coming in. Maybe you have a pension. Your portfolio is growing. Then required minimum distributions begin, and suddenly your taxable income jumps whether you need the money or not.1

For many households, that creates a painful chain reaction. More IRA withdrawals can mean a bigger tax bill, more of your Social Security becoming taxable, and higher Medicare premiums because of income-related adjustments.1 2 3

In this article, we will walk through a simple case study that shows why Roth conversions can matter so much in the years before age 73. We will also explain how to think about this strategy if you are within five years of retirement or already retired.

Why required minimum distributions can create a tax problem

Traditional IRAs are great while you are working because they help you defer taxes. The problem is that the IRS does not let that money sit there forever. In general, you must start taking required minimum distributions, or RMDs, from traditional IRAs beginning at age 73.1

Those withdrawals are usually included in your taxable income.1 That means even if you do not need the cash for living expenses, the distribution can still push you into a higher tax bracket.

Here is why that matters. Many retirees spend their 60s in a relatively lower tax window. They may have retired from full-time work, but they have not started RMDs yet. That can create a valuable planning gap. Once RMDs begin, that window often closes fast.

A simple example: how the tax squeeze shows up later

Let’s use a hypothetical retired couple, John and Jane, to show how this works.

They are both age 60 and recently retired. John has a modest pension paying about $1,700 per month. They want to spend about $8,000 per month in retirement. Most of their savings sit in a traditional IRA worth about $1.8 million, and they also have roughly $200,000 in a taxable brokerage account.

At first glance, this looks like a strong retirement plan. They have meaningful assets, reasonable spending, and multiple income sources.

The trouble shows up later.

Once RMDs start at age 73, the IRS requires annual withdrawals based on age and account balance.1 If the IRA has continued growing for more than a decade, the forced withdrawals can become large. In the planning example from the video, the couple’s effective tax rate stays fairly manageable in their early retirement years, then rises sharply once RMDs begin.

That spike is not caused by extra spending. It is caused by forced taxable income.

What higher taxable income can affect in retirement

The tax impact usually does not stop with the IRA withdrawal itself. Higher income can trigger problems in several places at once.

Tax issue | What happens | Why it matters |

|---|---|---|

Federal income taxes | RMDs are generally taxable as ordinary income.1 | More forced income can push you into a higher bracket. |

Social Security taxation | Up to 85% of Social Security benefits can become taxable when combined income rises above IRS thresholds.4 | A larger share of your retirement income gets exposed to tax. |

Medicare premiums | Higher-income retirees can pay added Medicare Part B and Part D premiums through IRMAA.3 | Your healthcare costs can rise even if your spending stays the same. |

Legacy planning | Many non-spouse beneficiaries must distribute inherited IRA assets within 10 years.2 | Children may owe significant income tax on inherited pre-tax money. |

This is why large pre-tax balances can become a hidden retirement risk. The account looks efficient while it is growing, but later it can create income that you no longer control.

Where Roth conversions fit in

A Roth conversion means moving money from a traditional IRA to a Roth IRA and paying tax on that amount in the year of the conversion. After that, the money can grow tax-free inside the Roth. Also, the original Roth IRA owner is not subject to lifetime RMDs.1

That is the big appeal.

Instead of waiting for the IRS to decide how much taxable income you must recognize in your 70s, you choose to recognize part of that income earlier, in years when your tax rate may be lower.

This does not mean every conversion makes sense. The goal is not to convert blindly. The goal is to convert strategically.

The best window for Roth conversions

For many retirees, the best time to look at Roth conversions is after full-time work ends but before RMDs begin.

That period can be powerful because:

Your earned income may be lower than it was during your working years.

Your RMDs have not started yet.

You may have more control over how much taxable income you recognize each year.

You may be able to convert enough each year to use up a lower tax bracket without spilling into a higher one.

In the video example, the strategy was to convert enough each year to fill the 22% tax bracket, but not go beyond it. The logic is simple. Pay tax at a rate you can live with now to avoid a potentially worse tax problem later.

What the case study showed

In the planning scenario from the video, John and Jane used annual Roth conversions before RMD age. When the couple’s results were compared side by side, the Roth conversion strategy produced a major long-term difference.

Scenario | Outcome in the case study |

|---|---|

No Roth conversions | Higher lifetime taxes and lower ending assets |

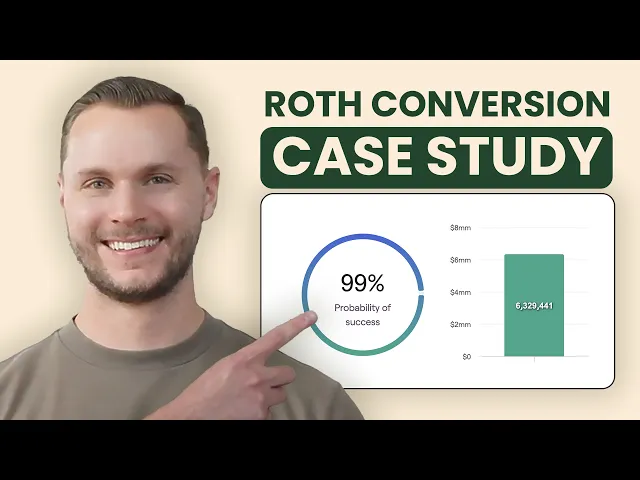

Strategic Roth conversions before age 73 | About $368,807 less in projected lifetime taxes and about $2,451,290 more in ending assets |

The video also showed a projected ending portfolio value of about $4.5 million without conversions versus about $6.3 million with conversions.

That does not mean every retiree will see numbers like these. They will not. Your result depends on your IRA balance, your filing status, your spending, your future tax rates, your Social Security timing, whether you have a pension, and what assets you are using to pay the conversion tax.

But the lesson is still important.

The tax cost of waiting can be much larger than many retirees expect.

How inherited IRAs raise the stakes

There is one more issue many families overlook.

If a large traditional IRA is left to children, many non-spouse beneficiaries generally must empty that account within 10 years, depending on their beneficiary status and other facts.2 If those children are in their peak earning years, those inherited IRA withdrawals may be taxed at high rates.

That means a retirement account that looked valuable on paper can create a heavy tax burden for the next generation.

A Roth conversion will not solve every estate planning issue, but it can change the tax character of the dollars you leave behind. That can make a meaningful difference for heirs.

When Roth conversions may be worth a closer look

Roth conversions are not automatic. Still, they are often worth reviewing if any of the following apply to you.

You have a large traditional IRA or old 401(k).

You expect RMDs to be larger than the income you actually need.

You are retired or close to retirement and currently in a lower tax bracket.

You want more control over future taxes.

You are concerned about Medicare premium surcharges.

You want to leave more tax-efficient assets to your family.

Common mistakes to avoid

A good Roth conversion plan is more precise than simply moving money to a Roth whenever the market is down.

Here are a few mistakes we often see:

Converting too much in one year

A large conversion can push you into a higher tax bracket and reduce the benefit of the strategy.

Ignoring the effect on Medicare premiums

Higher income can increase Medicare Part B and Part D costs through IRMAA, so conversion timing matters.3

Looking only at this year’s tax bill

The real question is not whether a conversion creates taxes today. It usually does. The real question is whether paying some tax now reduces your total lifetime tax bill.

Assuming the strategy is the same for everyone

It is not. A household with a pension, large IRA, and strong brokerage balance may have very different planning options than a household relying mostly on Social Security.

The bottom line

If most of your retirement savings are in pre-tax accounts, it is smart to look at your tax picture before age 73, not after.

That is often the window when you still have choices.

Roth conversions can help reduce future RMD pressure, lower the odds of a later tax spike, limit how much of your Social Security becomes taxable, and reduce the risk of higher Medicare premiums.1 3 4 Done well, they can also create more tax-free growth and leave more flexible assets for your family.

The key is to run the math based on your own numbers.

Want help seeing what this looks like for you?

If you want to understand whether Roth conversions make sense in your retirement plan, the next step is to model your real numbers. A good retirement analysis can show how IRA balances, spending, Social Security, pensions, and future RMDs may interact over time.

If you want a second opinion on your plan, Factor Financial can help you evaluate the right amount to convert each year so you are not paying more tax than necessary.

References

[1] Retirement topics - Required minimum distributions (RMDs ) | Internal Revenue Service

[2] Retirement topics - Beneficiary | Internal Revenue Service

[3] Benefits Planner: Retirement | Medicare Premiums | SSA

[4] Must I pay taxes on Social Security benefits? | Frequently Asked Questions | SSA

Zach Chiara, CFP®

See Our Planning Process